Bi-Weekly Payment Savings

See the impact of making half-payments every two weeks vs. one full payment monthly.

How This Tool Works

This calculator reveals the impact of making half-payments every two weeks instead of one full payment monthly. This simple change can shave years off your mortgage.

- Formula:

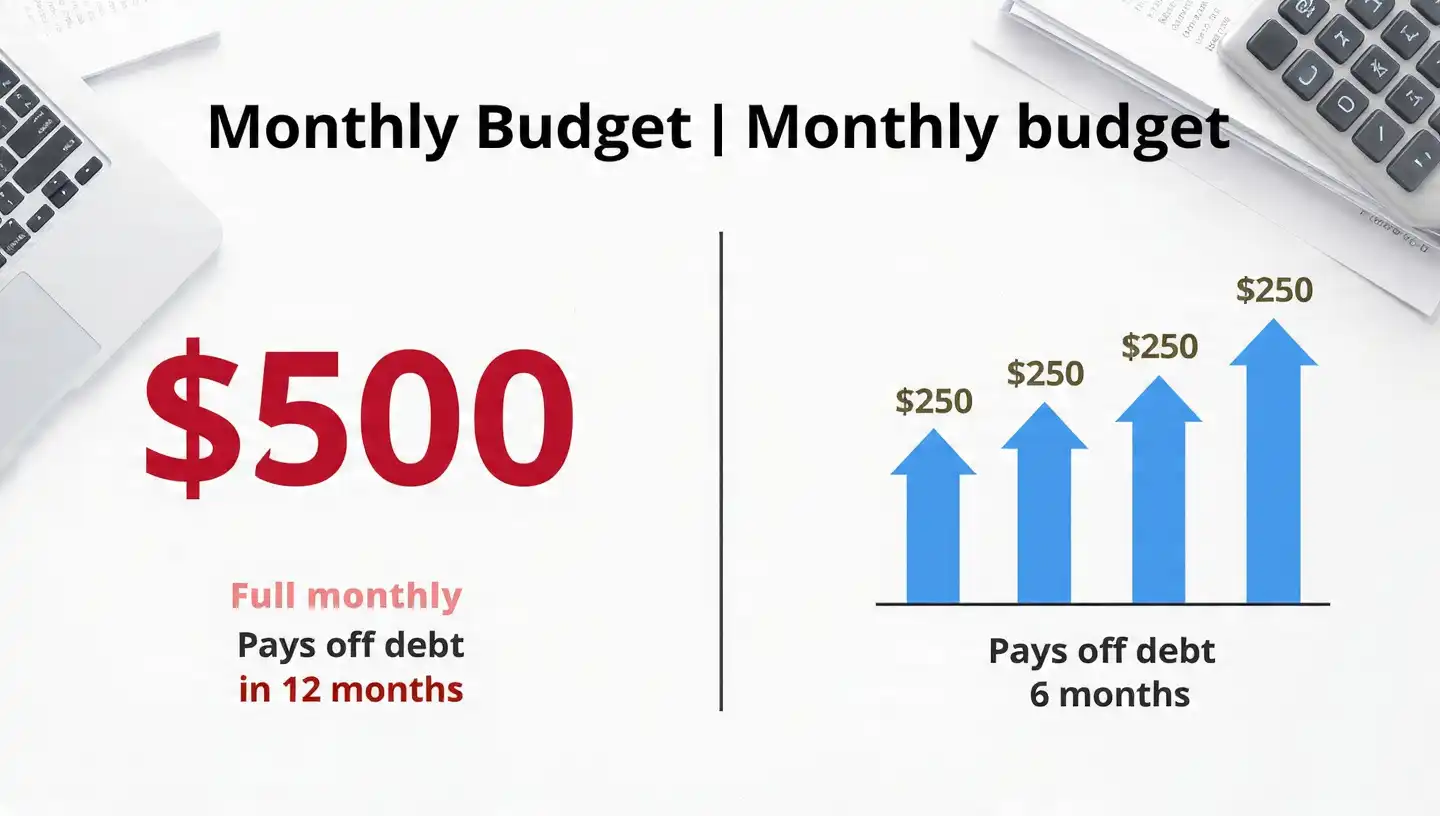

26 Half-Payments = 13 Full Payments per Year. - Logic: Since there are 52 weeks in a year, paying every two weeks results in 26 payments. This effectively means you make one "extra" full monthly payment every year, all of which goes directly toward reducing your principal.

- Assumptions: We assume your lender applies the payments immediately and does not hold them in a non-interest-earning account until the end of the month.

How to Use (Steps)

- Enter Loan Amount: Your current mortgage balance or the total amount you are borrowing.

- Enter Interest Rate: Your current or quoted annual interest rate (e.g., 6.5%).

- Enter Loan Term: The length of the loan in years (usually 30 or 15).

- Calculate: See your total interest savings and how much faster you'll pay off your home.

Example Calculation

Scenario: A $300,000 mortgage at 6.5% for 30 years.

• Monthly Payment: $1,896.

• Bi-Weekly Benefit: You make 13 payments/year instead of 12.

• Total Savings: ~$78,000 in interest.

• Time Saved: ~5 years and 8 months shaved off your loan.

• Verdict: You pay off the house in ~24 years instead of 30.

Why This Tool Is Accurate

Most homeowners don't realize that the "extra" payment is the engine of bi-weekly savings. This tool performs a full amortization comparison to show the compounding effect of reducing your principal balance faster than scheduled.

Limitations & Disclaimer

Some lenders charge a fee to set up a bi-weekly plan, or they may only apply payments monthly. Always check with your servicer first. Pro Tip: You can achieve the same result for free by just adding 1/12th of your payment to your monthly check.

Frequently Asked Questions

No, but you can "self-manage" it. Instead of a formal plan, simply pay your monthly amount plus an extra 1/12th each month. This has the exact same mathematical effect without the need for bank approval or fees.

If your mortgage rate is high (e.g., 7%+), paying it down is a guaranteed "return." If your rate is low (e.g., 3%), you might earn more by investing that extra payment in the stock market long-term.

Yes, any amortizing loan benefits from extra payments. However, since car loans are shorter (usually 5-7 years), the total interest savings will be much smaller than on a 30-year home mortgage.